Circuit breakers and lockdowns will eventually end but the world will be a different place after the coronavirus pandemic.

Specifically, we see the world becoming more indebted to the unprecedented policy rescue, less global as calls for localisation take hold, and more digital with greater adoption of key technologies.

These forces will have significant ramifications for investors. Outlooks for entire asset classes have changed. The preponderance of helicopter money and threat of higher inflation undermine the merit of holding government bonds but benefit inflation-protected bonds and gold. Stock picking will be affected by changes in consumer behaviour, corporate strategies and government regulations.

This creates a more volatile and challenging investment landscape. A diversified and nimble approach to investing is therefore crucial, as is keeping a close eye on the structural transformations at hand.

Debt is piling up globally as policymakers race to counter job losses and weakening balance sheets.

As a percentage of gross domestic product, we believe government debt could swell by 15 to 25 percentage points by the end of 2021, from pre-crisis levels across much of Europe and in the US.

Once the coronavirus is beaten, the focus will shift to how to pay for it all. Given Europe's bitter experience with populism after the 2008 financial crisis, austerity is unlikely. This leaves three options.

One, the costs of the bailouts could be socialised through financial repression. This occurs when governments suppress nominal yields and obligate captive pools of capital like pension funds, banks and insurers to hold government bonds.

Two, attempts may be made to inflate the debt away. Generating inflation hasn't proved straightforward in recent history. But sustained monetary policy largesse, coupled with a push towards localisation of select industries, could herald a period of moderately higher inflation once the global economy starts humming again.

Three, governments could seek to finance debt through higher taxes. Tying taxes to where revenues are earned appeals to a sense of fairness, not to mention nationalisation, by targeting foreign firms and technology companies. Higher taxes on capital gains, inheritance and wealth could also be on the cards.

For savers and investors, this would make long-term financial planning and considering after-tax performance even more important.

BOOST FOR AUTOMATION

This global lockdown has been an extraordinary experiment in extreme localisation, with billions of people banned from even leaving their own homes. And long after these measures are lifted, growing populist and protectionist voices worldwide will likely spur on the deglobalisation trend.

The US-China trade spat had demonstrated the dangers of long and complex global supply chains, and their vulnerability to changing geopolitical calculus.

Now with critical goods in short supply amid the Covid-19 fallout, companies and governments are rethinking their manufacturing footprint. For sectors deemed critical to national security, including medical supplies, drugs and food, local resilience will be prized over global efficiency. Supply chains will likely get shorter, more fragmented and more automated as a result.

Shifts in supply chains should lead to more investments in robotics, industrial software and automated factories and warehouses. This bodes well for the global automation and robotics market, whose share of global manufacturing revenues could rise from 1.5 per cent in 2019 to 6 to 8 per cent in the coming years.

Still, a mass exodus out of China is unlikely. According to the American Chamber of Commerce in China, over 80 per cent of US companies operating in China have no plans to relocate; the country still offers the best overall package in terms of cost, efficiency and reliability.

Instead, these companies are mostly adopting a "China plus" strategy: keeping their production bases there to serve the local market, while building incremental investments elsewhere, like in India, Malaysia and Vietnam.

Hence, while the global industrial reliance on China will decline over time, a total supply chain rejig remains a drawn-out process.

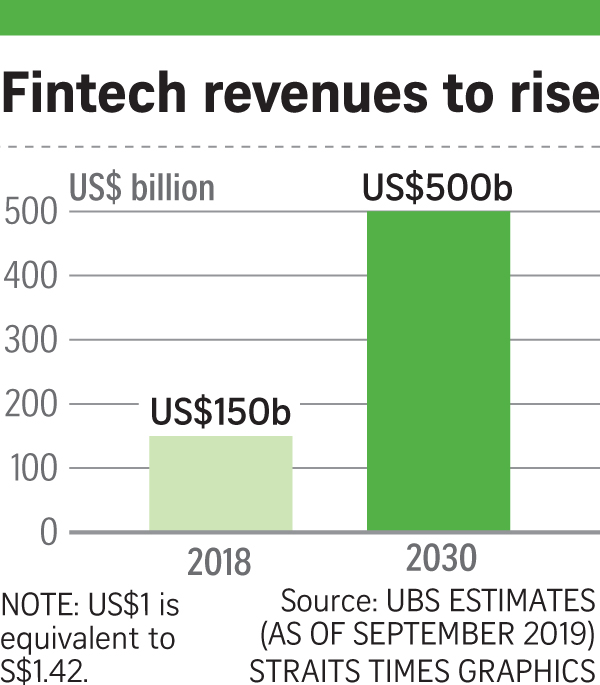

With quarantine measures in force, there has been a global lurch towards doing things online. Consumers staying home are taking to new digital platforms like e-commerce, video streaming, food delivery and online education.

In turn, this is hastening the shift to fintech-based digital solutions as such services are usually paid for via mobile or online platforms.

With the pandemic having exposed the shortcomings of many healthcare systems, this could be a driving force for healthtech, boosting demand for innovations like tele-medicine and health software, as well as developments in treatment methods, including genetic therapies and oncology.

INVESTMENT STRATEGIES

Global stocks, which are up over 25 per cent since their lows in March, could move even higher if signs point to the rapid development of a more sophisticated test and trace model or of effective medical solutions that can reduce the strain on healthcare systems.

Until then, we advocate a more selective approach. The impact of the recovery will be uneven and differentiated. Some firms are set to gain more clout, while others could take years to recapture pre-crisis profitability.

In equities, we prefer a combination of defensive blue chips, quality cyclicals and companies exposed to digital themes that have been accelerated by Covid-19. We also favour option strategies, such as put-writing, to earn a yield while pre-committing to buying on dips.

Credit offers a better risk-return profile overall than the other asset classes, in our view. We recently increased our allocation to US dollar investment-grade credit, which is backed by the Federal Reserve's buying and bondholder-friendly corporate behaviour such as suspensions to share buybacks, dividends and capital expenditures.

We also like US dollar high-yield credit and US dollar-denominated emerging market sovereign bonds. In Asia, we maintain a balanced exposure, with an overweight in Asian equities and Asian investment-grade bonds.

Talk of exiting lockdowns will likely excite markets in the near term. Yet, more importantly for investors, it is the pandemic's long-term outcome that will define future returns for years to come.

• The writer is Asia-Pacific head of UBS Global Wealth Management's chief investment office.