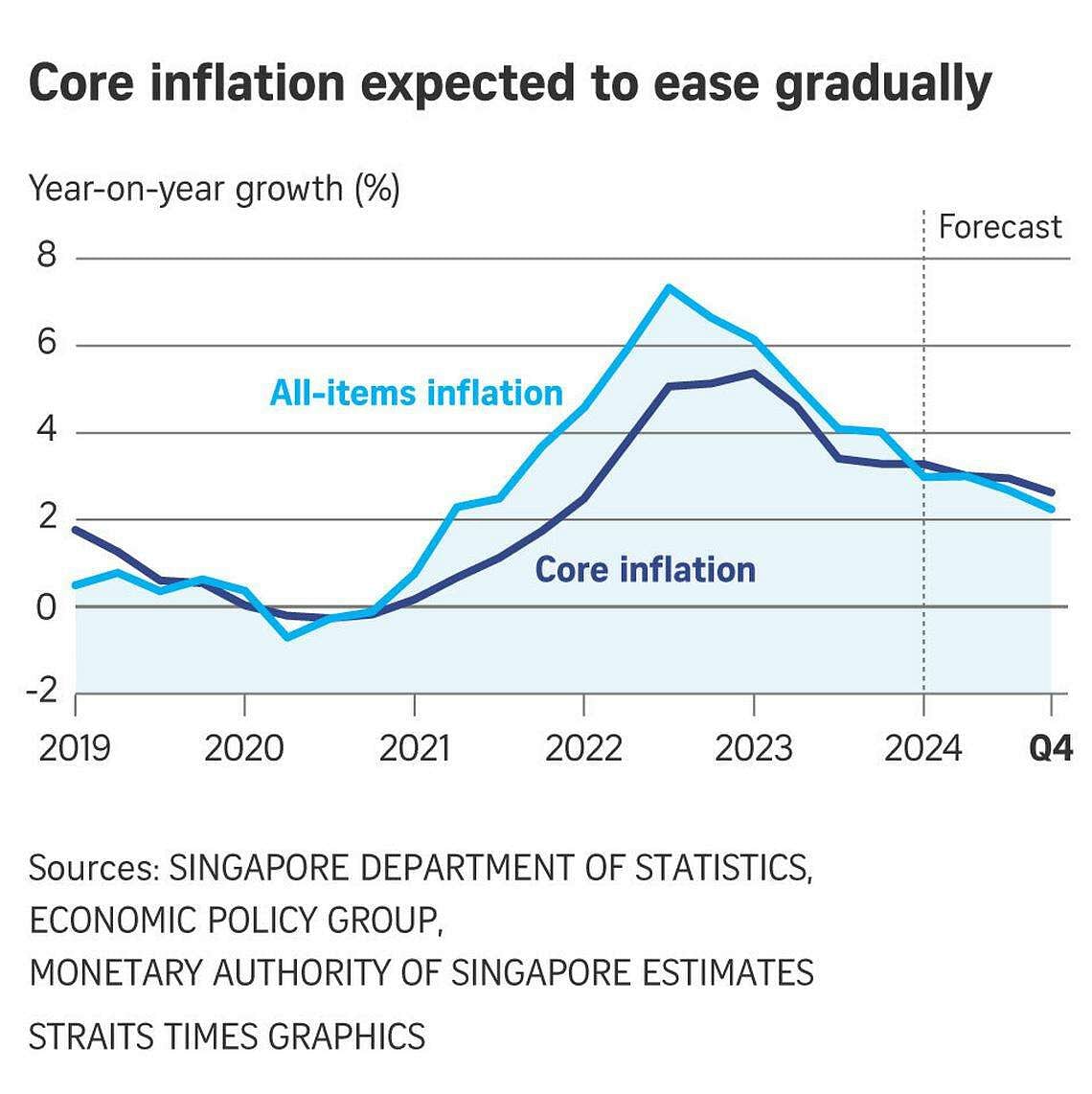

SINGAPORE - Core inflation in Singapore is expected to stay around 3 per cent in the near term, before “falling more discernibly” in the fourth quarter of 2024 and into 2025, the central bank said on April 26.

Consumer prices are likely to continue catching up with the higher cost levels in some goods and services for a while, the Monetary Authority of Singapore (MAS) said. This includes the step-up in water prices in April.

Hence, in the near term, core inflation – which excludes accommodation and private transport costs – will remain around current elevated levels. However, as the pass-through of accumulated costs to consumer prices progresses through the year, core inflation is projected to ease more meaningfully, MAS said in its macroeconomic review.

But it cautioned that inflation could also turn out to be stronger than anticipated due to global shocks to supply and demand.

For 2024 as a whole, MAS maintained its forecast for core inflation and headline inflation to average at 2.5 per cent to 3.5 per cent. Excluding the transitory effects of the increases in goods and services tax (GST), core and headline inflation are expected to come in at 1.5 per cent to 2.5 per cent.

MAS noted that the GST hike to 9 per cent has likely been fully passed through to most consumer prices as at March. While some residual pass-through remains due to some retailers’ choice to temporarily absorb the GST increase until later in the year, it is unlikely to raise inflation significantly in the upcoming months, it said.

Aggregate wage growth in the economy is also expected to moderate, with softer labour market conditions in the external-facing sectors.

“This should have a restraining effect on consumer demand, and consequently, the ability of businesses to raise prices strongly,” MAS said.

Certificate of entitlement premiums have also fallen markedly from 2023 levels, and the resulting drop in private transport inflation is expected to be the single largest driver behind the fall in headline inflation in 2024, it added.

Residential rental inflation should also moderate further as the supply of accommodation continues to rise, MAS said.

Core inflation came in slightly lower than expected in the first quarter of 2024, averaging 3.3 per cent, on the back of inflation for food and travel-related services slowing markedly. This offset the steeper pace of price increases for electricity and gas as well as other services.

“The elevated real exchange rate has also induced some residents to switch away from domestic spending to expenditure abroad. The softening labour market and the attendant slowdown in resident wage growth may also have weighed on consumer sentiment slightly,” MAS said.

Travel-related services inflation also eased in the first quarter of 2024, likely reflecting improved supply conditions in overseas tourist destinations, as well as the appreciation of the Singapore dollar, it added. Package tour fees dipped, driven in part by lower airfares as flight capacities to popular destinations increased.

However, unlike goods and travel-related services inflation, inflation in other services components picked up in the recent quarter, such as bus and train fares, taxi fares and education fees.

“Notably, these are also sectors for which labour shortages have remained acute and wage pressures strong,” MAS said.

Continuing with the disinflation trend, Singapore’s imported inflation as a whole is also expected to remain modest in 2024.

The inflationary impact of higher oil prices is, for now, expected to be contained and outweighed by easing inflation for other imported goods and services, MAS said. Specifically, global food-related commodity prices pertinent to Singapore’s consumption continued to fall in early 2024 as key markets remained well-supplied.

However, other global factors could also cause costs to go up again.

“Geopolitical tensions, especially in the Middle East, have intensified in recent weeks, and could pose risks to global energy prices,” MAS said.

“Should global energy prices rise further and stay at significantly elevated levels, the inflationary effects could extend beyond energy-specific consumer price index components as businesses facing higher utilities costs pass these on to consumer prices,” it said.

Meanwhile, on the demand side, a stronger-than-expected turnaround in the labour market towards the end of the year could also lift consumer sentiment and raise wage growth, it noted. This would in turn keep inflation elevated.

On the flip side, other scenarios such as the possibility of an unexpected weakening in the global economy could induce a faster easing of cost and price pressures, MAS added.

MAS also assessed that prevailing monetary settings remain appropriate, with core inflation expected to ease.

In January and April, MAS maintained the prevailing rate of appreciation of its Singapore dollar policy band.

“The sustained appreciation of the policy band would continue to dampen imported inflation and curb domestic cost pressures, thus ensuring medium-term price stability,” it said.