HONG KONG - Hong Kong’s ubiquitous Octopus payment system is encouraging users to switch from carrying only physical cards to having virtual wallets on their smartphones.

The company’s digitalisation push comes as it seeks to maintain its dominance amid intensifying competition in the city’s payment systems market.

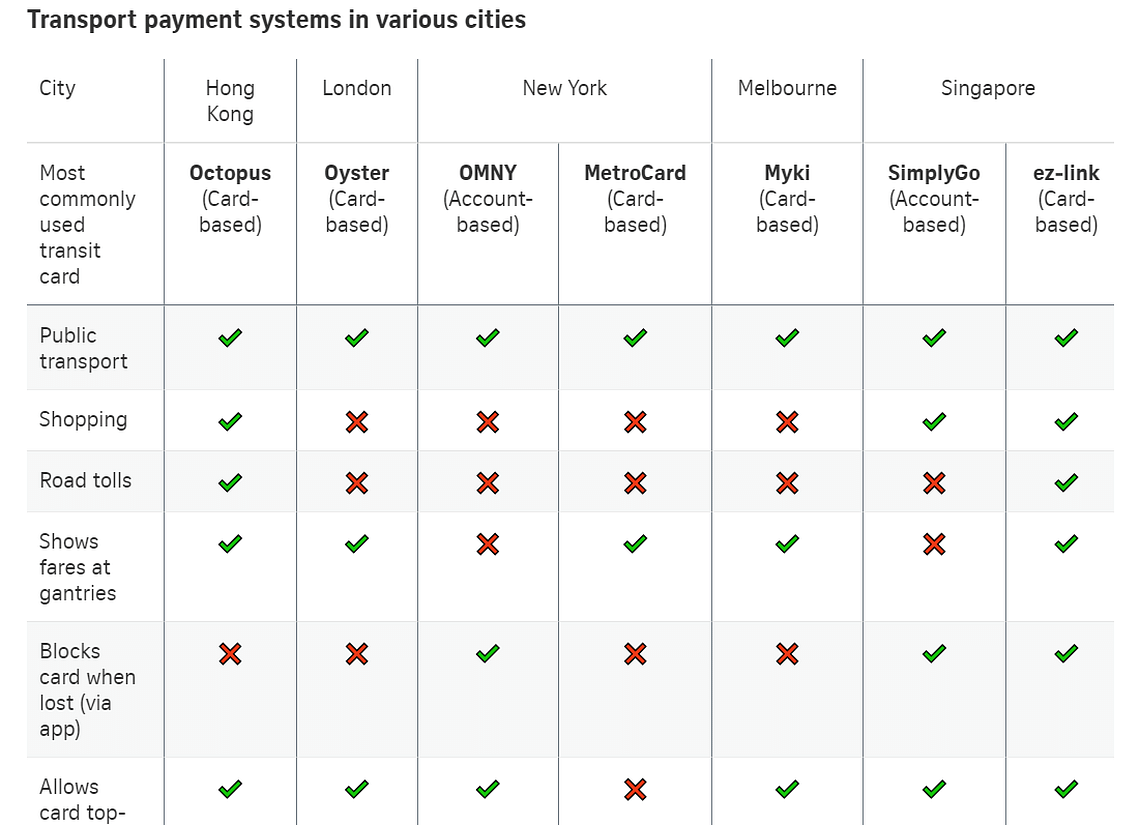

The Octopus card is an essential part of daily life in Hong Kong. Millions of residents use the contactless stored-value smart card to pay for virtually everything, from train rides to utility bills.

It also doubles as an access control card into schools, offices and residential buildings.

Its system boasts a turnover of HK$300 million (S$51.6 million) from 15 million transactions a day.

While Octopus has proven successful in the city since its launch in 1997, its chief operations officer Sammy Kam told The Straits Times that the company’s biggest present-day challenge was to nudge users into shifting their Octopus usage behaviour.

“We want to migrate our users from the traditional card-based system to the upgraded mobile-based one… so that we can make it fast, easy and convenient for our users to do everything from topping up their cards to deducting payment online through their mobile phones,” Mr Kam said.

Octopus chief executive Tim Ying told local media in October 2023 that the company aimed to bring its e-system to “every phone in every pocket” in Hong Kong.

More than one in five Octopus transactions are now generated by users of the mobile-based system, the company said in response to queries by ST, adding that it aims to have a majority of its users migrate to its mobile-based system for greater convenience in the near future.

Virtual Octopus cards became available on smartphones in Hong Kong around 2017, beginning with Samsung phones, then Apple iPhones and Huawei devices in 2020.

Users tap their phones against Octopus readers at railway turnstiles and retail stores to make payment, with the balance displayed immediately on the devices and the readers.

The Octopus app allows users to top up their physical and virtual cards on smartphones linked to their e-wallets, bank accounts or credit cards, as well as to make and receive payments using QR codes and a Faster Payment System (FPS) similar to Singapore’s PayNow system.

The virtual card can also work as a debit card in partnership with Mastercard and UnionPay.

On the mobile-based system, the Octopus app on each phone is associated with one account. A user can link more than one card to that account, listing one of them as the “default” card.

The default card’s data is then stored directly on the user’s phone chip using the proprietary Sony FeliCa near-field communication (NFC) technology.

If a user loses his smartphone, he can lock or unlink his Octopus account from his device’s cloud system, switch off the NFC service, and restore the Octopus account on a new phone.

Singapore’s EZ-Link travel card used the same NFC technology when it was first introduced, but the authorities later adopted the country’s own Cepas (Contactless e-Purse Application Specification) standard in 2009 to foster inter-operability between the competing EZ-Link and Nets CashCard systems.

The question of how other cities balance between upgrading their transport payment systems and losing functions such as the ability to reflect fare balances instantaneously has been debated in Singapore.

In January, Singapore pulled the plug on plans to phase out the EZ-Link card-based system for the SimplyGo account-based one.

The latter offers commuters wider e-payment options and more convenience, but was met with an outcry from commuters upset that fare balances were not displayed at MRT fare gates and bus readers.

Singapore said SimplyGo’s account-based system meant that travel records were held in a back office and transactions processed there, similar to how bank cards work.

It takes more time for the data to be transmitted back to the user, so showing fare balances at fare gates and bus readers would slow down the flow of commuters on public transport.

On Feb 5, it was announced that there were plans to make SimplyGo work for motoring payments down the road, on top of its current uses for public transport and retail.

According to Mr Kam, Octopus’ mobile-based system still uses NFC technology where ticketing is processed at fare gates and card readers.

But it also offers the option to enable Octopus-linked Mastercard or Union Pay prepaid cards that use account-based rules.

These let users receive push notifications of each transaction and their account balances on their mobile devices.

“At the end of the day, our biggest competitor is cash,” Mr Kam said. “The option of bank cards gives customers more choice, which is better for some users like tourists even if they can’t see their fare balances immediately.”

But Octopus’ main technology comes with its limitations too. Experts note that the Sony FeliCa NFC technology that Octopus uses is considered old, having been developed in 1988.

“The Sony FeliCa standard… is not as commonly supported globally compared with the more universal NFC standards such as ISO/IEC 14443 used by many other mobile payment systems,” Mr Emil Chan, co-chair of the Hong Kong Digital Finance Association, told ST.

Octopus’ reliance on the 35-year-old technology has meant that “compatibility with mobile phones and other devices is limited to those that support the Sony FeliCa standard”, said Mr Chan, who is also chairman of the Hong Kong Smart City Consortium’s fintech committee.

“Unlike transport cards issued by other cities such as Shenzhen and Guangzhou, the Octopus card cannot be virtualised and integrated in most mobile phones other than Apple, Samsung and Huawei devices… which can be a restriction for users who prefer using other smartphones,” he added.

Mr Kam, however, said it was Octopus’ customer-guided approach that led to its decision not to fix what was not broken and to instead expand its range of payment options for its consumers.

“The NFC tap-and-go contactless function is still Octopus’ core strength. Hong Kong people have shown that they prefer this over QR payments, especially for public transport, so we’ve done our part to give them what they want,” said Mr Kam, who has overseen Octopus’ implementation across Hong Kong since the 1990s.

A looming challenge for Octopus, Mr Chan said, was that its dominance in Hong Kong was increasingly being disrupted by super apps that offer a fuller buffet of services including e-payments, food delivery, messaging and social networking.

“The Octopus system faces competition from platforms such as Alipay and WeChat Pay, which have gained popularity in Hong Kong and can also be used across borders,” he said.

Hong Kong’s MTR train services started accepting QR code payments around 2020. AlipayHK has more than 3.3 million active users and WeChat Pay HK has over 5 million.

Octopus, meanwhile, says about 98 per cent of all Hong Kong residents aged 15 to 64 – more than 5 million people – possess an Octopus card.

“While Octopus in Hong Kong is highly versatile and widely used, it does not offer the diverse range of features and services typically associated with a super app, like WeChat in China, Grab in South-east Asia, and Gojek in Indonesia,” Mr Chan added.

Hong Kong’s Secretary for Transport and Logistics Lam Sai-hung suggested that Octopus’ success in the city over the years was not necessarily replicable given the fragmented market today.

“At the time (of Octopus’ launch in 1997), there were very limited electronic payment methods,” Mr Lam told ST.

“If we had to do the same today with all the current sorts of e-payments with their own markets, there would be more vested interests, and it would be much more difficult to unify them.”